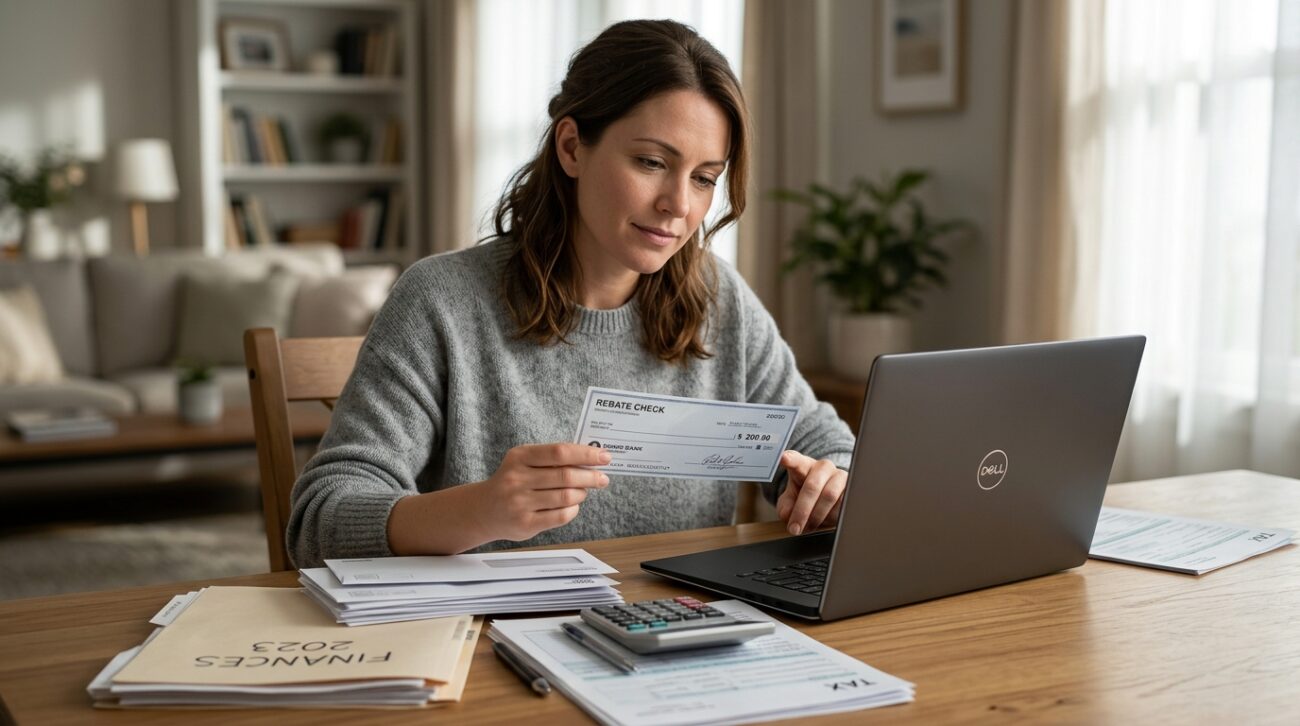

You just bought a new laptop, submitted a $200 mail-in rebate, and the check arrived three weeks later. Now you’re wondering: do I owe taxes on this? It’s a surprisingly common question, and the answer is less straightforward than most people expect.

The tax treatment of rebates depends on whether the payment reduces your purchase price or actually puts new money in your pocket. Get this distinction wrong and you could either overpay your taxes or underreport income — neither outcome is good. This guide breaks down exactly when a rebate is taxable, when it isn’t, and what the IRS says about the whole thing.

What Is a Rebate and Why Does It Matter for Taxes?

A rebate is a partial refund offered after a purchase. Retailers, manufacturers, and service providers use rebates as marketing tools to encourage buying without permanently lowering their listed price. You pay full price upfront, then receive money back through a check, prepaid card, or account credit.

For tax purposes, the core question is whether the rebate counts as income or as a price adjustment. That single distinction drives almost every rule discussed in this article.

Are Rebates Considered Taxable Income?

In most consumer situations, rebates are not taxable income. The IRS generally treats a rebate as a reduction in the purchase price of a product rather than a payment you earned. This position is grounded in the logic that you’re simply getting some of your own money back, not receiving compensation for work or investment.

The IRS addressed this directly in Revenue Ruling 76-96, which confirmed that cash rebates paid by manufacturers to customers are treated as purchase price reductions, not as income. So if you buy a car for $30,000 and receive a $1,500 manufacturer rebate, your actual cost basis becomes $28,500 — but you don’t report the $1,500 as income on your federal return.

This rule applies broadly to consumer product rebates — electronics, appliances, vehicles, and similar purchases.

However, there are situations where rebates cross into taxable territory, and knowing those exceptions matters.

Cash Rebates vs. Merchandise Rebates: Tax Differences

Not all rebates work the same way for tax purposes.

Cash rebates — including checks, direct deposits, and prepaid debit cards — are generally treated as price reductions. Because you paid money and received money back tied directly to that purchase, the IRS sees no net gain.

Merchandise rebates — where you receive a free product or gift card instead of cash — can be more complicated. If a rebate takes the form of a reward unrelated to the original purchase price, it may look more like a prize or promotional gift, which could be treated as taxable income under IRS rules for prizes and awards (governed by IRC Section 74).

For example, if a credit card company gives you a $500 gift card simply for opening an account — with no tied purchase — that amount is likely taxable and may be reported to you on a 1099-MISC or 1099-NEC. Credit card sign-up bonuses and cash-back rewards occupy a grey area that the IRS has not fully resolved, though most tax professionals treat them as non-taxable price reductions when tied to spending.

Manufacturer Rebates and Sales Tax

Here’s where many consumers and retailers get confused: sales tax on manufacturer rebates varies by state, and the rules are genuinely inconsistent across the country.

In some states, sales tax is calculated on the full pre-rebate price at the point of sale. You pay tax on $30,000 even though your net cost after a $1,500 rebate is $28,500. The rebate arrives later and is separate from the sales transaction, so the taxing authority sees the full amount as the sale price.

In other states, the rebate is deducted from the taxable sales price, meaning you only pay sales tax on the net amount after the rebate is applied.

The difference matters. On a $30,000 vehicle with a $1,500 rebate and a 7% sales tax rate, you’d pay $105 more in states that tax the full purchase price. Checking your specific state’s Department of Revenue guidance before finalizing a purchase can save you real money.

Rebates in Business Settings

When businesses receive rebates, the tax treatment shifts considerably. If a company buys inventory or equipment and receives a rebate, that rebate typically reduces the cost basis of the asset or the cost of goods sold. It is not treated as separate income.

However, if a business receives a volume rebate, loyalty rebate, or promotional allowance from a vendor, the timing and accounting treatment can affect taxable income. Under accrual accounting, a rebate may need to be recognized in the tax year it was earned, even if the cash hasn’t arrived yet.

Businesses claiming deductions for expenses that were later offset by rebates must adjust those deductions accordingly. Failing to reduce a deduction by a received rebate is an error the IRS may catch in an audit.

For businesses receiving large rebates — particularly in pharmaceutical, retail, or technology procurement — working with a CPA is advisable. The numbers are significant enough that the accounting treatment directly impacts quarterly estimated taxes.

State-Level Tax Rules on Rebates

Beyond sales tax, some states have specific income tax rules that differ from federal treatment. A handful of states follow the federal approach exactly, while others have enacted their own definitions of income that could bring certain rebates into taxable territory.

Most states with an income tax simply conform to federal adjusted gross income as a starting point, so if a rebate isn’t federal income, it generally isn’t state income either. But states like California and New York have complex tax codes with their own modifications, so it’s worth confirming with a local tax professional if large rebates are involved.

Common Scenarios Explained

Understanding abstract rules is easier with concrete examples.

Scenario 1 — Car Purchase Rebate: You buy a new SUV for $40,000. The manufacturer offers a $2,000 cash rebate. You receive a check after the sale. This is a price reduction. No federal income tax owed. Your cost basis is $38,000.

Scenario 2 — Appliance Rebate: You purchase a refrigerator for $1,200 with a $150 mail-in rebate offer. You submit the form and receive a prepaid Visa card for $150. Still treated as a price reduction. Not taxable income.

Scenario 3 — Credit Card Bonus: Your bank offers $300 cash back after spending $3,000 in the first three months. Most tax professionals treat this as a rebate on purchases — not taxable. The IRS has not issued a definitive ruling, but audits over credit card rewards are rare.

Scenario 4 — Bank Account Opening Bonus: A bank offers $400 for opening a checking account with no purchase requirement attached. This is not tied to spending, so it is treated as income. The bank will issue a 1099-INT or 1099-MISC. You owe ordinary income tax on it.

Scenario 5 — Business Volume Rebate: Your company receives a $10,000 year-end rebate from a supplier for hitting purchase thresholds. This reduces your cost of goods sold for the year. You adjust your deductions accordingly.

Conclusion

The tax on rebates question trips up a lot of people, but the underlying rule is actually simple once you understand it: if a rebate is tied directly to a purchase and reduces what you effectively paid, it’s not taxable income. If it’s money you received without a tied purchase, the IRS is more likely to treat it as income.

For everyday consumer purchases — cars, electronics, appliances — you almost certainly don’t owe any tax on your rebate. But for bank bonuses, business rebates, or any situation where a 1099 arrives in the mail, take a closer look before assuming it’s tax-free.

When in doubt, a quick conversation with a CPA costs far less than an IRS notice. Keep your receipts, understand your cost basis, and don’t leave money on the table by misreporting what you legitimately don’t owe.

FAQs

Do I need to report rebates on my tax return?

For most consumer rebates tied to product purchases, no — you do not need to report them. The IRS treats these as purchase price reductions, not income. However, bank account bonuses and some promotional rewards unconnected to a specific purchase must be reported as ordinary income.

Is a manufacturer rebate the same as a discount for tax purposes?

Functionally, yes. Both reduce the effective price you paid. The difference is timing — a discount happens at the register, while a rebate arrives afterward. For IRS purposes, both reduce your cost basis in the item rather than creating taxable income.

Does receiving a 1099 for a rebate mean I owe taxes?

If a company issues you a 1099-MISC or 1099-NEC for a rebate or promotional reward, they have reported that amount to the IRS. You should include it in your income unless you have a clear basis to exclude it — which is rare if a 1099 was issued. Consult a tax professional if the amount is significant.

Are credit card cash-back rewards taxable?

Generally treated as non-taxable rebates tied to purchases, not as income. The IRS has not issued a formal ruling requiring these to be reported, and major credit card issuers do not issue 1099 forms for standard cash-back rewards. Sign-up bonuses with no spending requirement are treated differently and may be taxable.

How do rebates affect the cost basis of a purchased asset?

A rebate reduces your cost basis in the asset. If you later sell the item, your capital gain (or loss) is calculated from the adjusted basis after the rebate. For high-value items like vehicles used in a business, this can have a meaningful impact on depreciation calculations.